Life Insurance With Cash Value Disadvantages

High administrative fees and service fees for managing investment accounts.

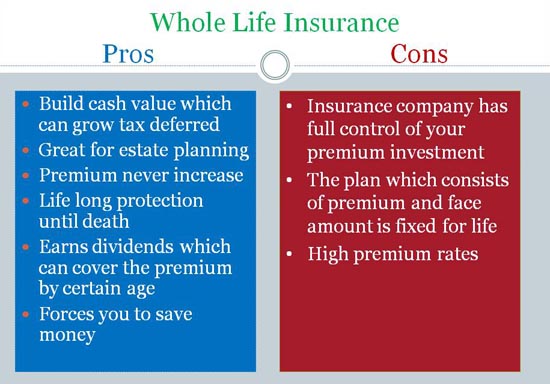

Life insurance with cash value disadvantages - Types of permanent life insurance include whole life universal life and final expense insurance which is a form of whole life. However our primary focus at i e is on permanent cash value life insurance. People who want to access their cash value can borrow it from this account tax free in most cases as well.

Cash value life insurance has been a big controversy amongst financial planners over the years. So interest on a cash value policy account grows without the policyholder having to claim it on their taxes. Death benefit payouts are tax free in most cases.

Most of the disadvantages of cash value life insurance are associated with costs and coverage limitations. Things to consider with cash value withdrawals. But before we begin a brief introduction into the different types of.

So the majority of the article on the advantages and disadvantages of life insurance will be focused there. Some say it is a great tool because you can build a retirement account to offset your retirement income on a tax free basis. First withdrawing money from the cash value may increase your premium payments thus making the policy more expensive.

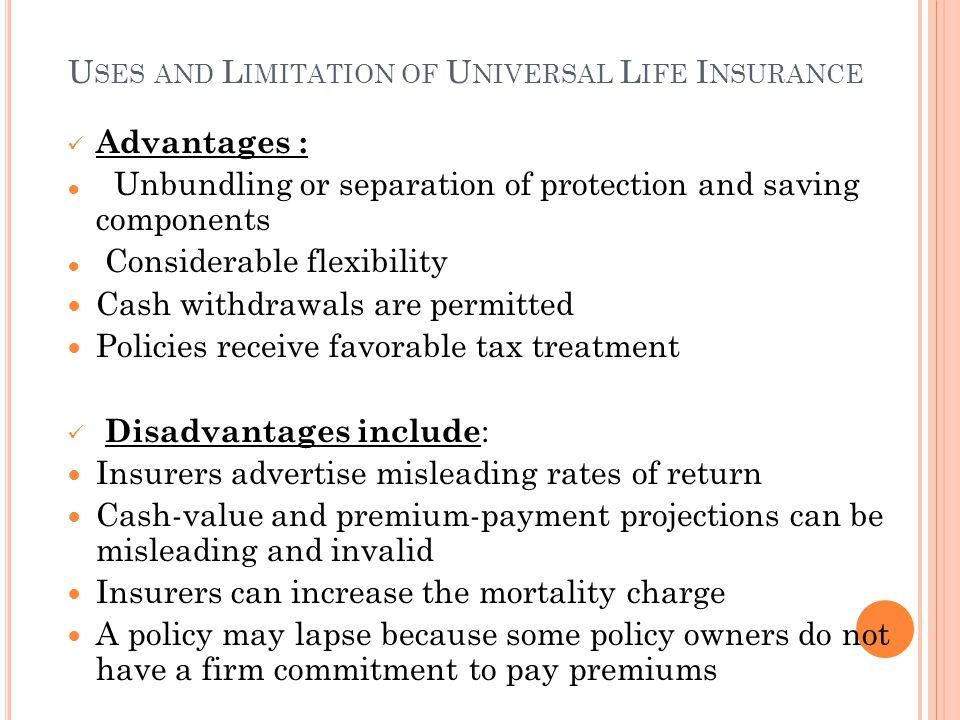

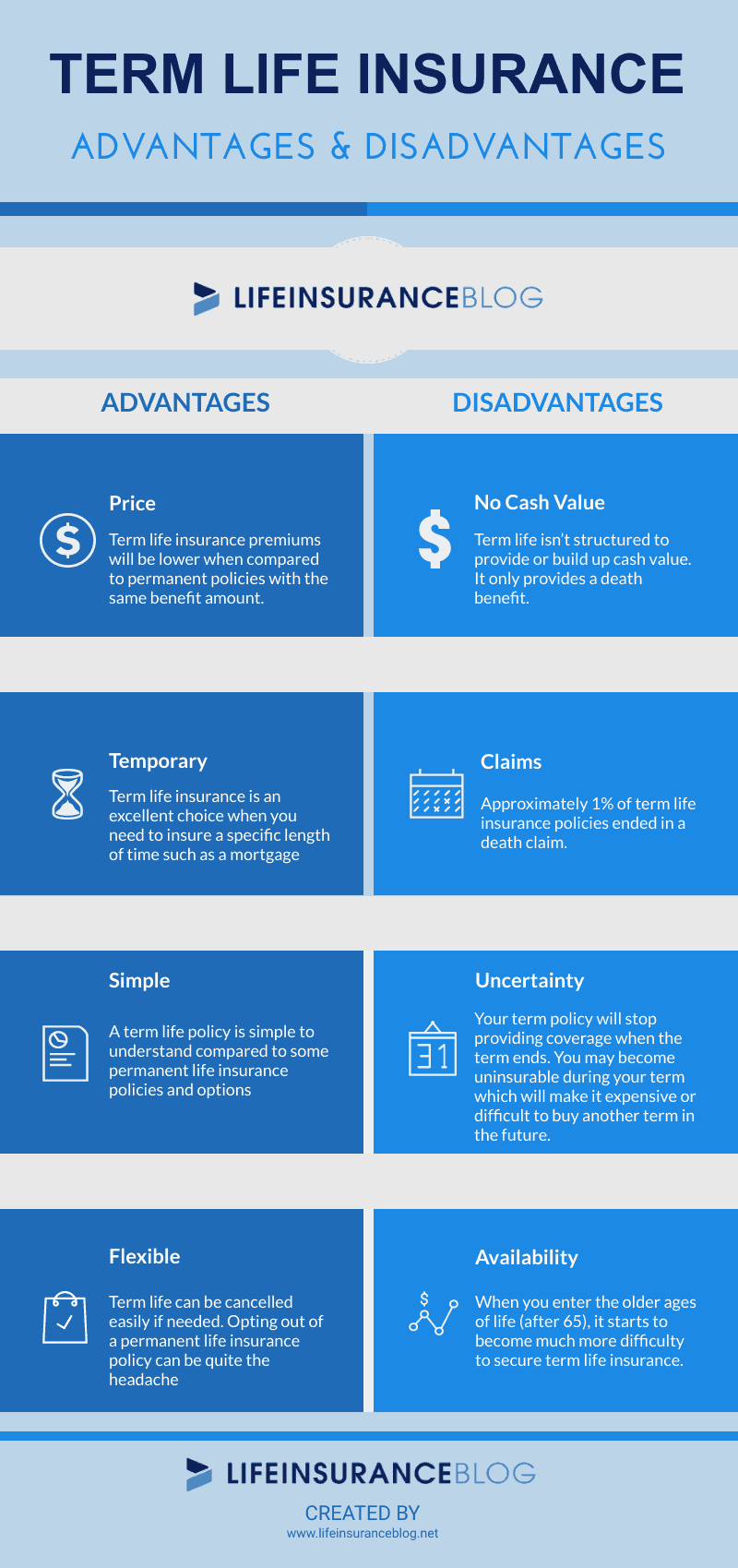

Term life policies eventually expire have no cash value and usually don t provide any benefits if the insured does not die during the term though a few term policies have riders allowing for partial payouts in. Additionally a life insurance policy also allows for tax free cash value growth. Depending on your insurance company they will determine whether you are eligible to borrow against your cash value or not.

Yearly price of protection method. There are many life insurance benefits worth talking about. Some lenders require at least 60 months of paid premiums while others require 120 months which is equivalent to 10 years of insurance payment.

And if you can t afford the new higher premiums then the policy could lapse. The yearly price of protection method is used to find out the cost of. A method used in actuarial analysis which is often used in the insurance industry.

Growth of your cash value can be tied to an index such as the s p 500 indexed universal life insurance or sub accounts that contain investments you choose variable universal life. Looking at the advantages and disadvantages we can clearly state that cash value insurance though comparatively more expensive than term life can be a sigh of relief for the policyholder when he is alive and is in term of need of money but on a death benefit ground it is a loss because the policyholder is paying more money for almost 3 4 times. It is important to understand a couple of key disadvantages that come with this alternative.